Insurance Tiers Explained: How They Control Your Medication Costs

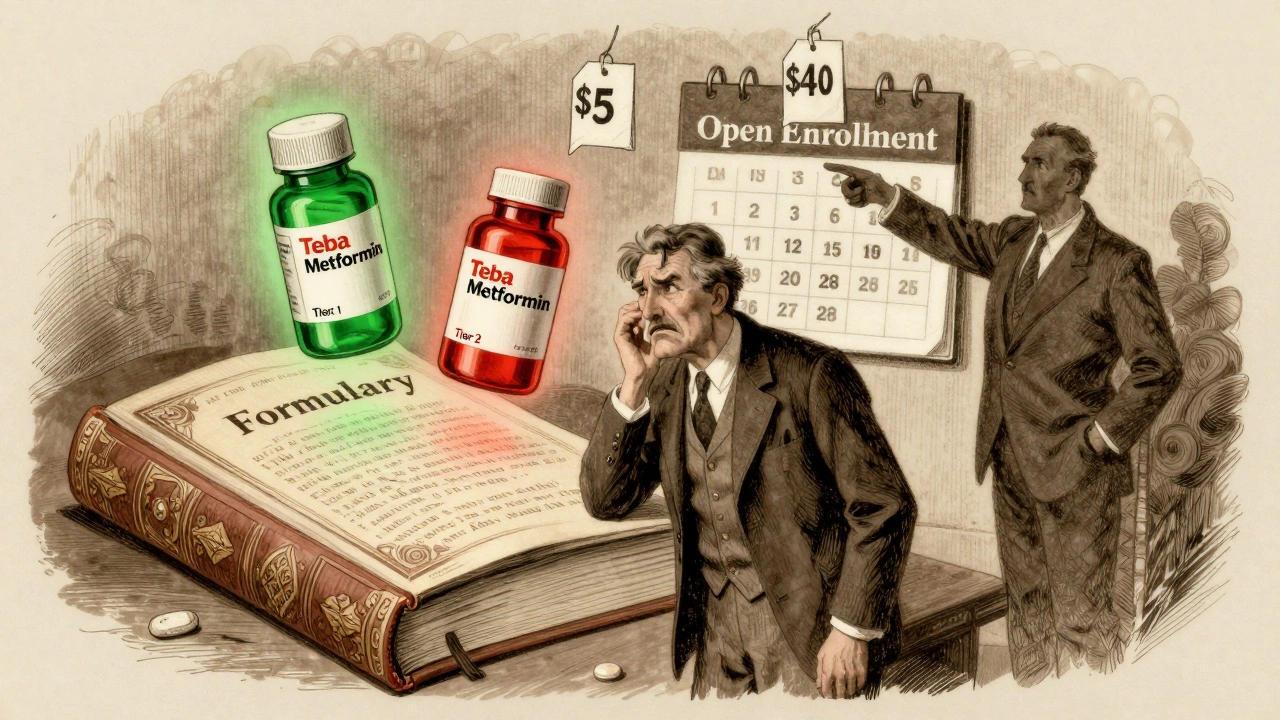

When you pick up a prescription, the price you pay isn’t just set by the drug company—it’s decided by your insurance tiers, a system that groups prescription drugs into levels based on cost and preference. Also known as drug formulary tiers, this structure tells your plan how much to cover and how much you owe. It’s not random. Every drug you take is placed into one of these tiers, and that single decision can mean the difference between paying $5 or $500 a month.

Most plans have four to five tiers. Tier 1 is usually generic drugs—the cheapest, most common options. Tier 2 is preferred brand-name meds, Tier 3 is non-preferred brands, and Tier 4 is specialty drugs like biologics for conditions like rheumatoid arthritis or cancer. But here’s the catch: just because a drug is on your plan doesn’t mean you get it cheap. Prior authorization, a requirement where your doctor must prove a drug is medically necessary before the plan pays. Also known as pre-approval, it’s often used for expensive drugs on Tier 4 or 5 to block unnecessary spending. And if your drug isn’t on the formulary at all? You might pay full price—or be forced to switch.

Medicare Part D plans use the same system, and they’re required to cover at least two drugs in every therapeutic category. But that doesn’t mean you’ll get the one your doctor recommends. Many plans push patients toward cheaper alternatives—even if those alternatives don’t work as well. That’s why knowing your plan’s tier list matters. A drug like Humira might be on Tier 4, but its biosimilar could be on Tier 2, cutting your cost by 70%. Drug formulary, the official list of medications covered by your insurance plan. Also known as preferred drug list, it’s updated every year, and your plan isn’t required to tell you until open enrollment. If your med got moved from Tier 2 to Tier 3 last year, your copay just jumped—and you might not have noticed until you got to the pharmacy.

Insurance tiers aren’t just about cost—they’re about control. Plans use them to steer you toward cheaper drugs, often before your doctor even considers alternatives. That’s why reading your plan’s formulary isn’t optional. It’s your first line of defense against surprise bills. And if you’re on long-term meds for diabetes, high blood pressure, or mental health, a single tier change can wreck your budget. The good news? You can appeal. You can ask for a tier exception. You can switch plans during open enrollment. But you have to know what you’re up against.

Below, you’ll find real-world guides on how to fight back. From understanding why your biosimilar was denied to learning how to check your plan’s formulary before you fill a script, these posts give you the tools to take control. No jargon. No fluff. Just what actually works when insurance tiers are working against you.

Switching Health Plans? How to Check Generic Drug Coverage to Save Money

Switching health plans? Don't overlook generic drug coverage. A small change in formulary tiers can cost you hundreds or thousands annually. Learn how to check your meds, compare tiers, and avoid surprise costs.